Critical Minerals Are Becoming a Semiconductor Supply Chain Risk

Critical minerals are moving from the background of the semiconductor conversation to the center of supply chain strategy. On June 18, Reuters reported that China defended its export controls on critical minerals after the G7 pledged to reduce reliance on Chinese supplies and increase coordinated stockpiling. The G7 plan includes efforts to reduce dependence on any single non G7 supplier to below 60% by 2030, with longer term movement toward 50%. (Reuters)

Critical minerals are moving from the background of the semiconductor conversation to the center of supply chain strategy. On June 18, Reuters reported that China defended its export controls on critical minerals after the G7 pledged to reduce reliance on Chinese supplies and increase coordinated stockpiling. The G7 plan includes efforts to reduce dependence on any single non G7 supplier to below 60% by 2030, with longer term movement toward 50%. (Reuters)

For semiconductor manufacturers, this is an important signal. The risk is no longer limited to finished chips, wafers, or fab capacity. It is moving further upstream into the minerals, materials, gases, chemicals, and processing inputs that make semiconductor production possible.

Why Critical Minerals Matter to Semiconductors

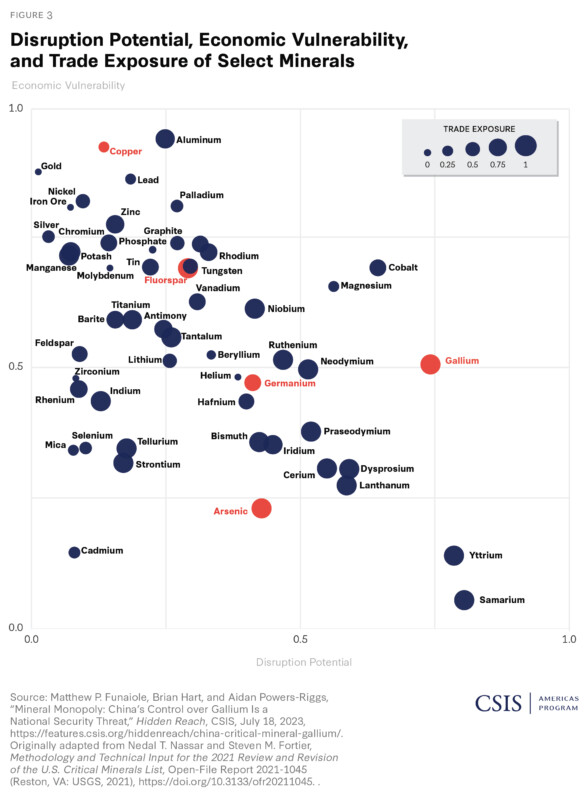

Semiconductors depend on a wide network of upstream materials. Rare earths, graphite, gallium, germanium, antimony, lithium, nickel, cobalt, and copper all support different parts of the electronics, energy, defense, and semiconductor ecosystem. Some are used directly in chipmaking. Others are essential for semiconductor equipment, magnets, batteries, power systems, and advanced manufacturing infrastructure.

This creates a layered supply chain risk. A company may have access to a chip supplier, but that supplier still depends on upstream materials. If those inputs become restricted, delayed, or more expensive, the impact can move downstream quickly.

China remains a dominant player in many of these supply chains. Reuters reported earlier this year that China refines between 47% and 87% of copper, lithium, cobalt, graphite, and rare earths, according to the International Energy Agency.

Why Export Controls Change the Risk Profile

Export controls create a different type of disruption than a normal shortage. In a shortage, supply may be limited because of demand, production capacity, or logistics. With export controls, access can depend on licensing, policy decisions, and geopolitical conditions.

That makes planning harder.

Companies cannot always solve this kind of risk by finding another supplier quickly. Critical mineral processing is complex, concentrated, and difficult to replicate. Even when alternative reserves exist, mining, refining, qualifying, and scaling supply can take years.

This is why the G7 is focusing not only on alternative sources, but also on coordinated stockpiling, recycling, data sharing, and market risk alerts through the International Energy Agency.

The Semiconductor Supply Chain Is Moving Upstream

For OEMs and EMS providers, the larger lesson is clear. Semiconductor risk does not begin when a part goes on allocation. It begins much earlier.

It can begin with mineral extraction. It can begin with refining. It can begin with specialty materials, equipment, or components that support chip production. By the time disruption reaches the finished component market, options may already be limited.

This is why procurement teams are paying closer attention to upstream signals. Critical minerals policy, export licensing, stockpiling initiatives, and material concentration are becoming part of semiconductor supply chain planning.

Where Storage Fits Into the Bigger Picture

As upstream risks grow, inventory planning becomes more strategic. Companies may need to secure critical semiconductor components, wafers, die, or related materials earlier in the lifecycle. Once secured, that inventory must be preserved correctly.

Semiconductors are sensitive to moisture, electrostatic discharge, temperature variation, contamination, and handling conditions. Poor storage can turn protected inventory into unusable inventory.

Controlled semiconductor storage helps maintain component integrity through humidity control, ESD protection, stable environmental conditions, traceability, and documented handling. In a market shaped by export controls and material concentration, storage becomes part of how companies protect access over time.

The Bigger Lesson

Critical minerals are no longer just a mining or policy issue. They are now a semiconductor supply chain issue.

As governments respond with stockpiling plans and diversification targets, manufacturers will need to understand how upstream material risk affects downstream availability. The companies best positioned for this environment will be those that look beyond finished components and plan around the full supply chain.

Semiconductor resilience now depends on more than fabs. It depends on materials, processing, storage, and long term supply control.