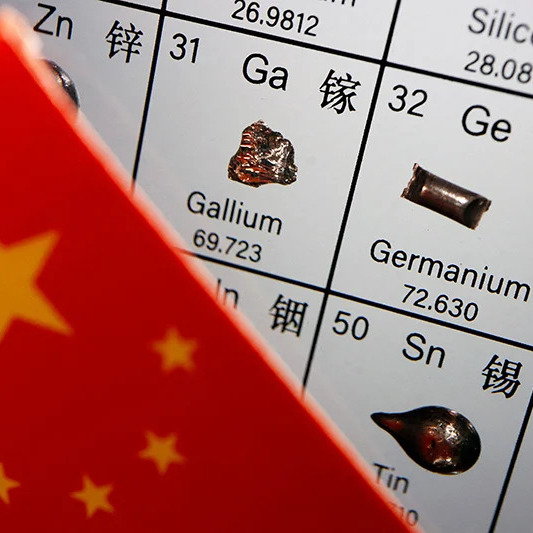

China’s Gallium and Germanium Export Ban: Implications for Semiconductor Supply Chains

China’s recent decision to ban the export of gallium and germanium, along with their chemical compounds, has sent ripples through the global semiconductor industry. As key materials used in semiconductors, electric vehicles, military defense systems, and display technologies, this restriction introduces challenges that could reshape supply chains and spur regional production innovations.

China’s recent decision to ban the export of gallium and germanium, along with their chemical compounds, has sent ripples through the global semiconductor industry. As key materials used in semiconductors, electric vehicles, military defense systems, and display technologies, this restriction introduces challenges that could reshape supply chains and spur regional production innovations.

Why Gallium and Germanium Matter

Gallium and germanium are vital in advanced semiconductor manufacturing. Gallium is commonly used in gallium arsenide (GaAs) chips for high-speed electronics, while germanium is a critical component in photonics and solar cell technologies. Both materials are by-products of processing other commodities, such as bauxite and coal, making them resource-intensive to produce. With China as the dominant producer of these metals, its export restrictions could lead to a shortage of these essential materials in the global market.

Potential Supply Chain Impacts

The immediate impact of the ban is uncertainty. While current suppliers report no disruptions yet, the long-term effects could include:

- Increased Costs: With limited supply, prices for gallium and germanium are expected to rise, encouraging investment in alternative production methods.

- Regional Production Shifts: Other countries may scale up production to offset the restrictions, leading to diversification in sourcing.

- Innovation in Recycling: Increased focus on recovering gallium and germanium from existing products may emerge as a cost-effective alternative.

Strategic Resilience in Semiconductor Storage

As the industry navigates these changes, secure storage and warehousing solutions for critical materials like gallium and germanium become paramount. Building regional stockpiles and optimizing storage practices can mitigate immediate risks, ensuring uninterrupted access to these components during supply chain adjustments.

Looking Ahead

China’s export ban highlights the vulnerability of concentrated supply chains. The semiconductor industry must prioritize diversification, regional production, and innovative material recovery to adapt to this evolving landscape. Proactive storage strategies and sourcing adjustments will be key to maintaining stability in a rapidly changing market.